{kind=link}

The “Finish Hedge Fund Management of American Properties Act” is as harmful because the invoice’s identify is deceptive: Hedge funds don’t management American Properties; certainly, they’re a minority of whole single-family actual property funding by way of each properties purchased and {dollars} spent. The invoice, looking for to make amendments to the Inner Income Code of 1986, introduces a punitive excise tax on sure taxpayers who fail to liquidate their single-family actual property holdings.

Whereas laws aimed toward addressing the housing scarcity is way wanted, singling out massive institutional buyers is, frankly, little greater than scapegoating. Certainly, by denying households which are unable to afford mortgage entry to rental items and successfully banning most other ways of funding a house buy, this laws guarantees to make the housing market much more dysfunctional than it at the moment is.

Understanding the Laws

On the core of the invoice is Chapter 50B, a brand new addition to the tax code, which might impose a 50% tax on the “truthful market worth” of newly acquired single-family residences for relevant taxpayers, ramping up over the following teen years when it will lastly take full impact. Part 5000F, nevertheless, takes a distinct route by penalizing those that fail to satisfy particular necessities associated to extra single-family residences by imposing a hefty $50,000 multiplied by the surplus variety of owned residences over a specified restrict. Guidelines regulating what constitutes an “extra” are stipulated in Part 5000G.

Part 5000G defines phrases, establishes aggregation guidelines, and mandates reporting to the Secretary whereas outlining penalties for non-compliance. In the meantime, Part 3 introduces a housing down-payment Belief Fund, funded by the imposed taxes, which is then earmarked for down-payment help grants.

After all, the laws is extraordinarily obscure. It doesn’t define who precisely will qualify for this down-payment help. That stated, these tax penalties are so Draconian that there’ll seemingly be no significant amount of cash ever positioned on this fund. The laws is, successfully, a authorities ban on corporations proudly owning greater than 50 homes of single-family actual property masquerading as a tax.

The Laws and Taxation

The laws locations a fifty-thousand-dollar tax on properties owned by hedge funds—permitting them to go untaxed on 90% of the variety of properties they at the moment personal within the first 12 months, 80% the second 12 months, and many others. till finally all properties are taxed. Equally, it applies an almost an identical tax on all different massive holders of single-family properties—with the exception that these entities are allowed to personal fifty properties, with the “extra” making use of solely to the variety of properties owned over fifty. After ten years, this 50,000 greenback per residence tax would get replaced by a tax of fifty% of the house’s “truthful market worth.” In the long term, this could be tantamount to instituting a fifty-home cap on all single-family actual property buyers.

The invoice does, fortunately, exempt banks holding foreclosed properties and builders whose properties usually are not at the moment leased to anybody: With out these exceptions, the invoice may by accident set off a banking disaster or stop practically all new single-family housing development. That stated, its results on the housing market would, on internet, be dangerous. Certainly, given its present wording, the invoice perversely incentivizes hedge funds speculating in single-family actual property to carry onto their properties with out renting them as a result of unoccupied properties usually are not topic to the confiscatory 50% tax.

Speculations Round The Laws

After all, speculating on rising property values by shopping for and holding the land with out leasing it to tenants will solely cut back the provision of housing nonetheless additional. A coverage that leaves completely advantageous properties unoccupied is an inherently inefficient one. After all, there are causes to avoid wasting property for future use, however an asset that housing can usually depreciate sooner when it’s not occupied as points with the property go unnoticed and worsen.

Most of the articles complaining in regards to the “downside of hedge fund hypothesis” level out that many hedge funds are shopping for property in minority neighborhoods. Which means the proposed laws may have the unintended impact of denying individuals who reside in these areas entry to single-family leases: The smaller landlords that the laws favors are extra seemingly than bigger landlords to have interaction in red-lining, just because it’s more durable to show within the case of smaller land-holders—simply as it’s more durable to show racial bias within the case of smaller employers. (Simply so you already know, I’ve nothing towards small companies and imagine the overwhelming majority are owned by good, truthful individuals. I see each massive and small companies as enjoying a worthwhile position within the economic system.

My level is simply about provability.) Many households dwelling in these areas discover themselves, no less than quickly, unable to afford a mortgage and wish entry to those rental properties.

Hedge Funds Are Not the Reason behind the Affordability Disaster

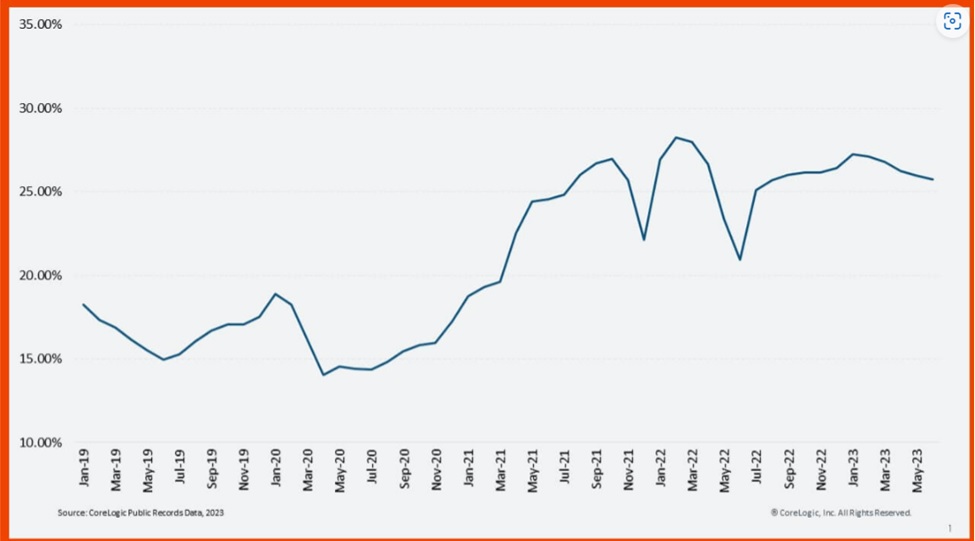

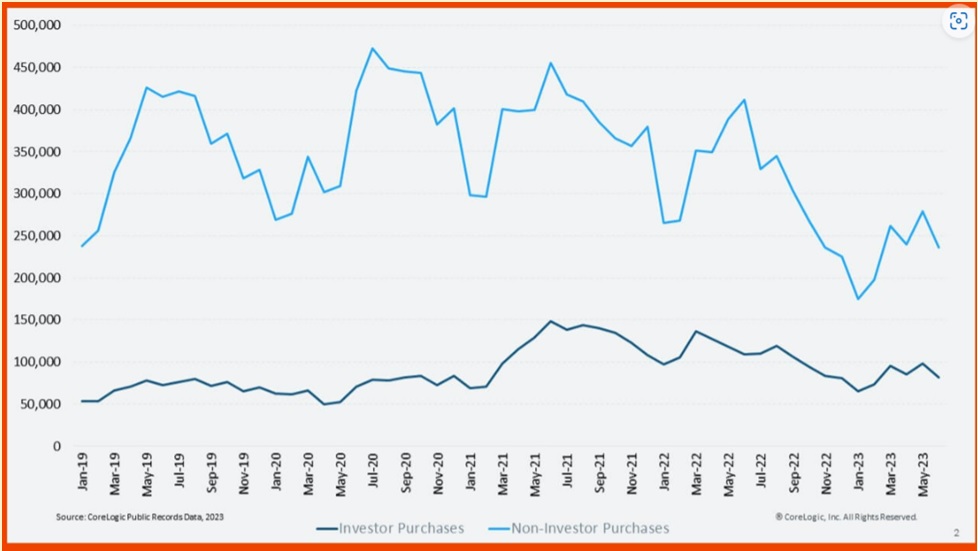

Hedge funds make up solely a fraction of funding purchasers. And funding purchases, whereas excessive by historic requirements (although they’re off their 2022 peak), nonetheless represent solely a fraction of all residence purchases.

Housing provide and demand have fallen collectively—because the locked-in impact makes owners unwilling to promote and excessive rates of interest make patrons unable to purchase: Certainly, the choice to promote your own home and purchase a brand new one is, within the present market, successfully a call to refinance right into a massively greater rate of interest. In absolute phrases, investor exercise can also be down, as the next graph illustrates.

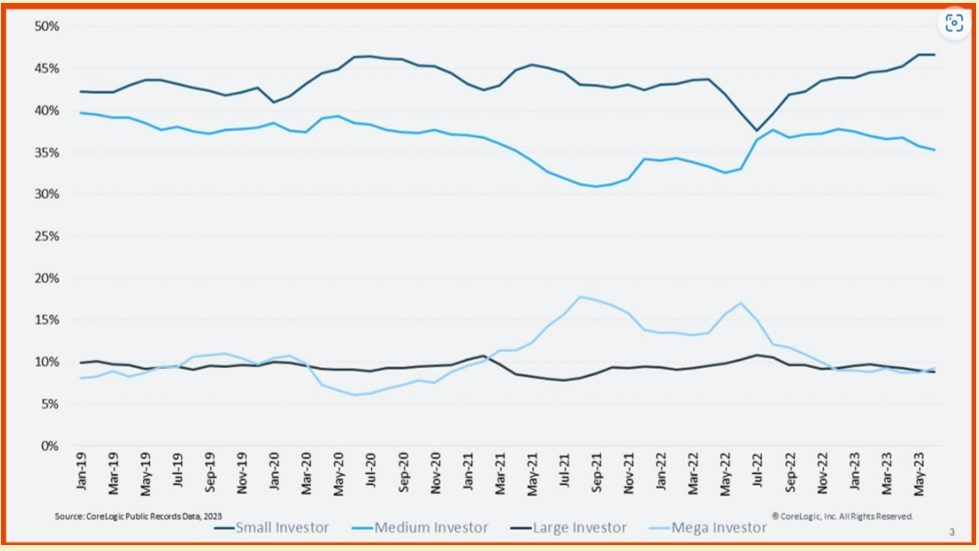

If mega-investors are pricing out common patrons, why aren’t additionally they pricing out smaller buyers? Small buyers make up a bigger share of funding purchases, whereas the mega-investors have turn into a smaller one. It’s laborious to imagine that an actor who’s lowering its exercise out there is by some means chargeable for the affordability disaster.

Conclusion

The true drivers of the affordability disaster are 1) excessive rates of interest and a couple of) limitations on new development—with limitations on new development being the extra long-standing, and extra essential, trigger. Rates of interest will finally come down, however we now have no motive to imagine that constructing new properties will turn into any simpler as time goes on. After all, native governments profit from decrease populations and elevated residence costs as they search to maximise per capita income: This perverse incentive should be handled if housing is ever to turn into reasonably priced once more. (See my article on housing affordability.)

The “Finish Hedge Fund Management of American Properties Act” is a essentially misguided piece of laws. Whereas the laws could also be well-meaning, in actuality, it merely scapegoats institutional buyers and reduces the obtainable inventory of single-family, standalone rental housing. It’s going to solely make the issue worse.

The “Finish Hedge Fund Management of American Properties Act” Is Critically Misguided was final modified: December twenty first, 2023 by

Franklin Carroll

Franklin Carroll is Kukun’s VP of Modelling and Analytics; After ending his research on the College of Chicago, he labored at Fannie Mae the place he helped construct Collateral Underwriter, roll out the Worth Confirm initiative, and specialised in collateral associated and credit score associated coverage.

Revealed December 21, 2023